The Role of Open Banking and Financial Data Sharing in Securing Better Loan Terms

Summary

Let’s be honest. Applying for a loan can feel like a black box. You hand over your pay stubs, bank statements, and credit score, then wait for a faceless algorithm to pronounce its judgment. It’s frustrating. But what if you […]

Let’s be honest. Applying for a loan can feel like a black box. You hand over your pay stubs, bank statements, and credit score, then wait for a faceless algorithm to pronounce its judgment. It’s frustrating. But what if you could open that box? What if you could actively use your own financial data to negotiate, to prove you’re a good bet, and to literally unlock better rates?

Well, that’s the promise of open banking. It’s not just a tech buzzword—it’s a fundamental shift in power. And it’s quietly revolutionizing how we secure everything from personal loans to mortgages.

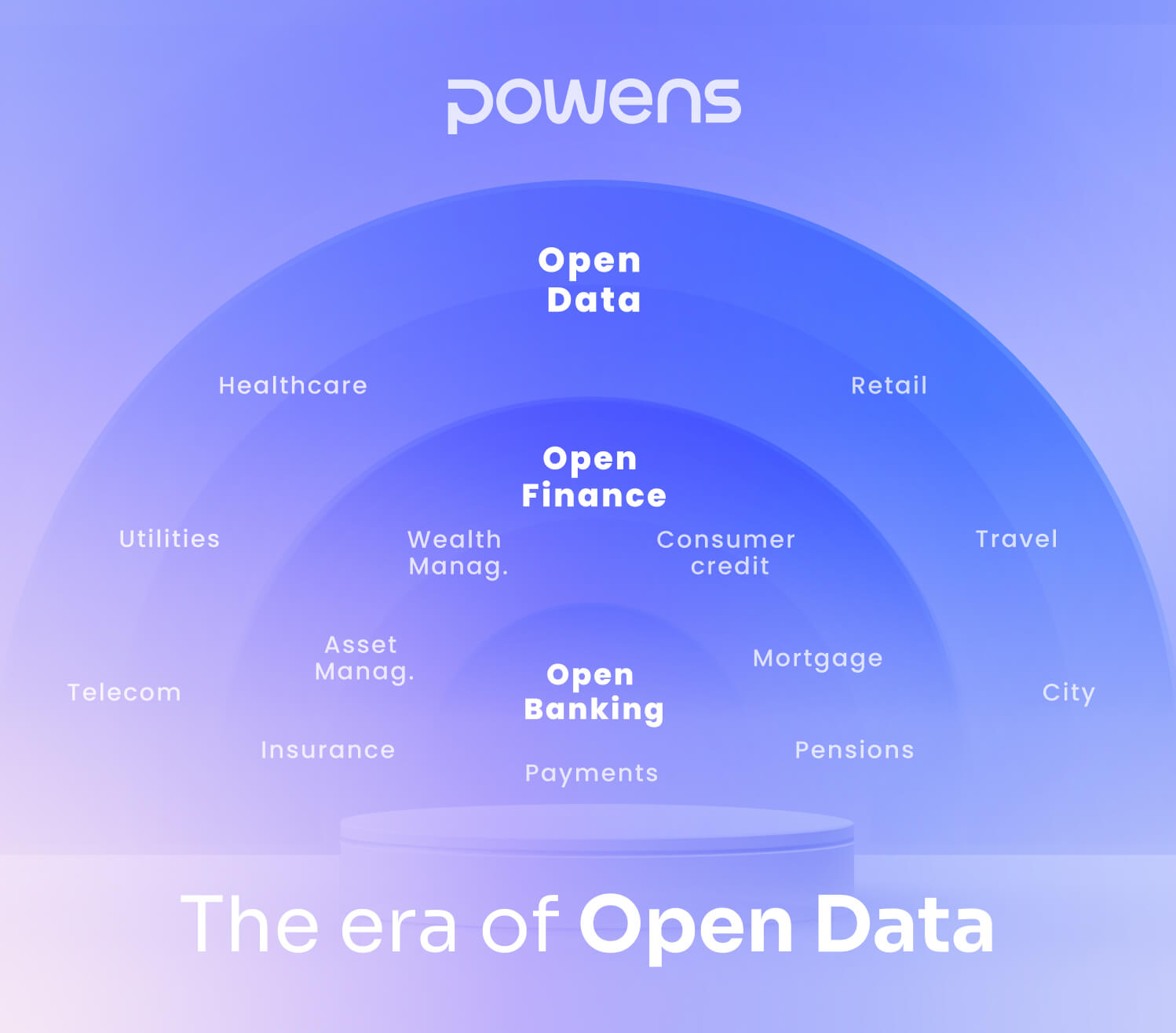

What Is Open Banking, Really? Let’s Demystify It.

Think of your financial life as a series of isolated islands. Your checking account is on one island. Your investment app is on another. Your utility payments? They’re stranded somewhere else. Traditional lenders only get a blurry satellite image of one or two of these islands (usually your credit report and submitted statements). They miss the whole archipelago.

Open banking, with your explicit consent, builds bridges between these islands. It allows secure, API-driven sharing of your financial data between your banks and authorized third parties—like a loan provider you’re applying to. You’re not just showing a snapshot; you’re granting a real-time, verified tour of your entire financial landscape.

The Core Shift: From Credit Score to Cash Flow Reality

Here’s the deal. Your credit score is a history of your debt. It tells a story, sure, but it’s an incomplete one. It doesn’t see your consistent rent payments, your healthy savings habit, or your steady freelance income that hits your account like clockwork. For millions—the self-employed, gig workers, or those rebuilding credit—this is a massive pain point.

Open banking changes the narrative. It enables cash flow underwriting. Lenders can analyze your actual income and spending patterns. They see your true financial discipline, not just your debt history. This is a game-changer for securing favorable loan terms.

How Sharing Your Data Actually Gets You a Better Deal

It feels counterintuitive, doesn’t it? Sharing more feels risky. But in this case, transparency is your strongest asset. Here’s how it translates to tangible benefits on your loan application.

1. You Become More Than a Number

By sharing your transaction data, you provide context. A lender might see a dip in your score but also see you’ve never missed a rent payment in five years and have a solid emergency fund. That context can move you from a “decline” or “high-risk” category into an “approved” one—often at a lower interest rate than you’d get otherwise.

2. Faster, More Accurate Applications

Gone are the days of hunting down PDF statements or waiting for paper mail. Open banking verifies your income and assets instantly. This speed reduces friction for the lender and, honestly, for you. A smoother, verified application can sometimes be viewed more favorably—it signals organization and legitimacy.

3. The Power of Personalized Offers

With a fuller picture, lenders can tailor offers. They might see you consistently save 20% of your income and offer a slightly larger loan amount with confidence. Or, they could offer a dynamic repayment plan aligned with your irregular income cycles. This level of personalization was simply impossible before.

The Practical Steps: Using Open Banking for Your Next Loan

Okay, so how do you actually do this? It’s becoming easier every day.

- Look for Lenders That Offer It: Many fintech lenders and even traditional banks now have “open banking” or “verify instantly” options during their online application process. It’s often a button that says something like “Connect your bank account securely.”

- You Are Always in Control: Remember, you must give explicit, one-time consent. You choose which accounts to share and for how long. You can revoke access at any time. The data is shared read-only—no one can move your money.

- Prepare to Showcase Your Strengths: Before you apply, think about which accounts best tell your financial story. Maybe it’s your primary checking for income, a savings account for reserves, and even a utility account to show stability.

| Traditional Loan App | Open Banking Loan App |

|---|---|

| Relies on credit score & static documents | Uses real-time cash flow & transaction data |

| Manual verification (slow) | Instant, automated verification |

| “One-size-fits-all” risk assessment | Personalized, nuanced risk profile |

| Limited context for financial behavior | Full context for income, spending, and stability |

Navigating the Concerns (They’re Valid)

Security and privacy are the big, obvious questions. And they should be. The ecosystem is built on strong data protection regulations (like GDPR in Europe and similar principles elsewhere). Data is encrypted, shared via secure APIs, and never stored unnecessarily by the third party. You’re not giving away your login credentials; you’re granting a temporary, permissioned access token.

The other concern? Will sharing more hurt me if my spending isn’t perfect? Possibly. But in many cases, lenders are looking for patterns of responsibility, not perfection. A few impulsive buys are normal; the overall trend is what matters. It’s about presenting a truer you.

The Bottom Line: A Fairer Financial Future

Open banking, at its heart, is about democratizing data. Your data. For decades, financial institutions held all the cards—and the information. Now, you can wield that information to advocate for yourself.

Securing better loan terms is no longer just about having a pristine credit history. It’s about demonstrating your real-world financial health. It’s about turning your daily financial habits—the ones your credit score never sees—into your strongest reference. That’s a profound shift. It turns data sharing from a vulnerability into a strategic tool. And that, well, changes everything.