Implementing Statistical Arbitrage and Pairs Trading with Retail Brokerage Tools

Summary

For years, statistical arbitrage and pairs trading felt like the exclusive playground of hedge funds with supercomputers and PhD quants. The math is complex, sure. The data demands are huge. But here’s the deal: the toolkit available to the retail […]

For years, statistical arbitrage and pairs trading felt like the exclusive playground of hedge funds with supercomputers and PhD quants. The math is complex, sure. The data demands are huge. But here’s the deal: the toolkit available to the retail trader has evolved—dramatically. You can now implement a version of these strategies from your laptop. It’s not about replicating a billion-dollar fund. It’s about applying a disciplined, mean-reversion framework to your own portfolio.

What Are We Actually Talking About? A Quick Primer

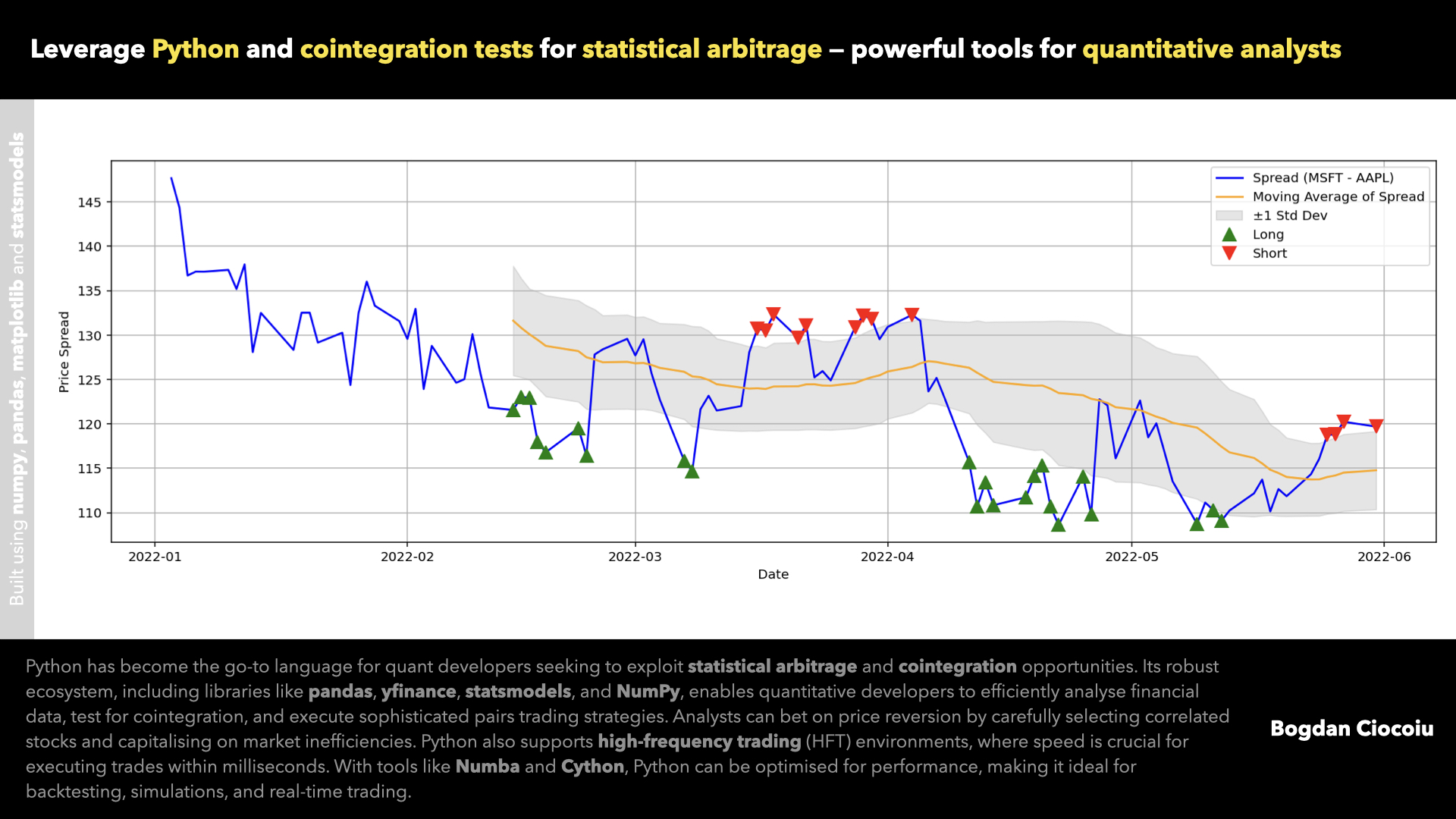

Let’s strip away the intimidation. Pairs trading is the simpler cousin. You find two stocks that historically move together (like Coca-Cola and Pepsi, or two oil majors). When their price ratio strays too far from its historical norm—one stock gets too “expensive” relative to the other—you short the outperformer and buy the underperformer. You’re betting on the gap closing.

Statistical arbitrage (“stat arb”) expands this idea. It uses quantitative models to identify fleeting price discrepancies across dozens, even hundreds, of securities. It’s a high-frequency, multi-legged game of equilibrium. For us retail folks, a multi-pair strategy is often the practical entry point. The core principle for both? Mean reversion. Markets overreact, then they correct.

The Modern Retail Trader’s Arsenal: It’s More Than Just a Chart

Honestly, the biggest shift hasn’t been in theory, but in access. Your average brokerage platform is now a data powerhouse. Here’s what you should be looking for—and using.

Screening & Backtesting Tools

You can’t just guess pairs. You need to find correlated assets. Screeners in platforms like Thinkorswim, TradingView, or even your broker’s advanced tools let you filter by sector, market cap, and—crucially—run correlation studies. Find stocks with a high historical correlation (say, above 0.8). That’s your starting universe.

Backtesting is your safety net. Most platforms now offer some form of it. You can test your simple pairs logic: “Buy Stock A, Short Stock B when the spread hits 2 standard deviations.” See how it would have performed over the last 5 years. Did it survive the 2020 crash? The results will humble you, fast.

Spread Charts & Custom Indicators

This is the secret weapon. Many charting packages allow you to create a ratio chart (Stock A / Stock B) or a spread chart (Stock A price minus a multiplied Stock B price). Plotting this ratio with Bollinger Bands or a Z-score indicator visually shows you the extremes—the entry and exit zones. It turns abstract math into a visual trading signal.

Execution & Risk Management Features

Pairs trading is a market-neutral strategy, ideally. You want your profit to come from the spread narrowing, not from the overall market’s direction. To manage this, you need:

- Bracket Orders: To enter both legs simultaneously. A market move while you’re only half-in can wreck your risk profile.

- Beta-Weighting: Some platforms (looking at you, Thinkorswim) let you view your portfolio risk in terms of a benchmark. It helps you see if your “market neutral” pair is actually neutral.

- Real-time Margin Calculators: Because shorting one leg uses margin. You must know your buying power impact before you click.

A Step-by-Step Walkthrough for Your First Pair

Let’s make this concrete. Imagine you’re using a common retail platform. Here’s a simplified flow.

1. The Hunt for a Relationship

Start in the same sector. Technology? Look at AMD and NVIDIA. Consumer staples? Target and Walmart. Use the correlation function on their price series over the last 2-3 years. A high correlation is your foundation. But—and this is key—also check for a fundamental reason they should move together. Don’t just rely on blind stats.

2. Modeling the Spread

Create a ratio chart (Stock A/Stock B). Normalize it so it’s easier to read. Add a 20-day moving average and 2 standard deviation bands. Your trading rule becomes: Short the ratio (i.e., short A, buy B) when it touches the top band. Go long the ratio (buy A, short B) when it hits the bottom band. Exit when it crosses back to the mean.

| Signal | Action | Bet On |

| Ratio hits +2 Std Dev | Sell Stock A, Buy Stock B | Ratio decreasing (spread narrowing) |

| Ratio hits -2 Std Dev | Buy Stock A, Sell Stock B | Ratio increasing (spread narrowing) |

| Ratio crosses 20-day MA | Close entire position | Mean reversion complete |

3. Execution & The Real-World Snags

You’ve got your signal. Now, log into your brokerage and use a bracket order to enter both sides at once. Use a limit order to get a decent fill. This is where theory meets friction: slippage, bid-ask spreads, and commission (if any) eat directly into your thin profit margin. Size small. Your first trade is a learning exercise, not a retirement plan.

The Inevitable Pitfalls (And How to Sidestep Them)

This isn’t a free lunch. Far from it. The market has a nasty habit of breaking patterns just when you’ve committed capital.

The Correlation Breakdown: This is the big one. Two stocks can decouple forever due to a company-specific event—a scandal, a breakthrough product, bankruptcy. Your “mean” is gone. That’s why you need a hard stop-loss on the individual legs, not just the spread. If one stock gaps against you 20% on news, the historical relationship is probably void.

Transaction Cost Drag: You’re making many trades for small gains. If you’re paying even $1 per trade, it adds up. Factor this into your backtest. Honestly, it kills more strategies than market risk does.

Timing and Patience: The spread can widen… and keep widening. Your capital is tied up in a losing position that should revert. It’s a psychological grind. You’ll question your model. Having the historical backtest data is the only thing that might keep you in the seat.

Is This Still Viable for the Retail Trader?

Well, yes and no. The low-hanging fruit is gone. The pros are doing this with nanosecond advantages you can’t touch. But as a framework for disciplined, non-directional trading? Absolutely. It forces you to think in terms of relationships and value, not just green and red candles. It teaches rigorous risk management.

The tools have democratized the process, not the edge. Your edge now comes from your patience, your portfolio construction, and your ability to adapt. Maybe you apply pairs logic to ETFs instead of volatile single stocks. Perhaps you focus on longer timeframes to avoid the high-frequency noise. You use the retail brokerage tools to build a systematic approach in a world of emotional reactions.

In the end, implementing statistical arbitrage concepts with your retail account is less about printing money and more about cultivating a quantitative mindset. It’s about learning to listen to the subtle, statistical hum of the market—and knowing when that hum has hit a discordant note worth betting against. The real profit might just be in the education.