Navigating the Tax Maze: Your Guide to HSAs and High-Deductible Health Plans

Summary

Let’s be honest—taxes and health insurance are two topics that can make anyone’s eyes glaze over. But when you combine them? Well, it can feel like deciphering a secret code. That’s where Health Savings Accounts (HSAs) and High-Deductible Health Plans […]

Let’s be honest—taxes and health insurance are two topics that can make anyone’s eyes glaze over. But when you combine them? Well, it can feel like deciphering a secret code. That’s where Health Savings Accounts (HSAs) and High-Deductible Health Plans (HDHPs) come in. They’re a powerful, and honestly, often misunderstood duo that can seriously impact your financial health.

Here’s the deal: getting a grip on the tax implications isn’t just about saving a few bucks at filing time. It’s about building a smarter, more resilient financial future. So, let’s dive in and untangle this knot, one thread at a time.

The Dynamic Duo: How HSAs and HDHPs Work Together

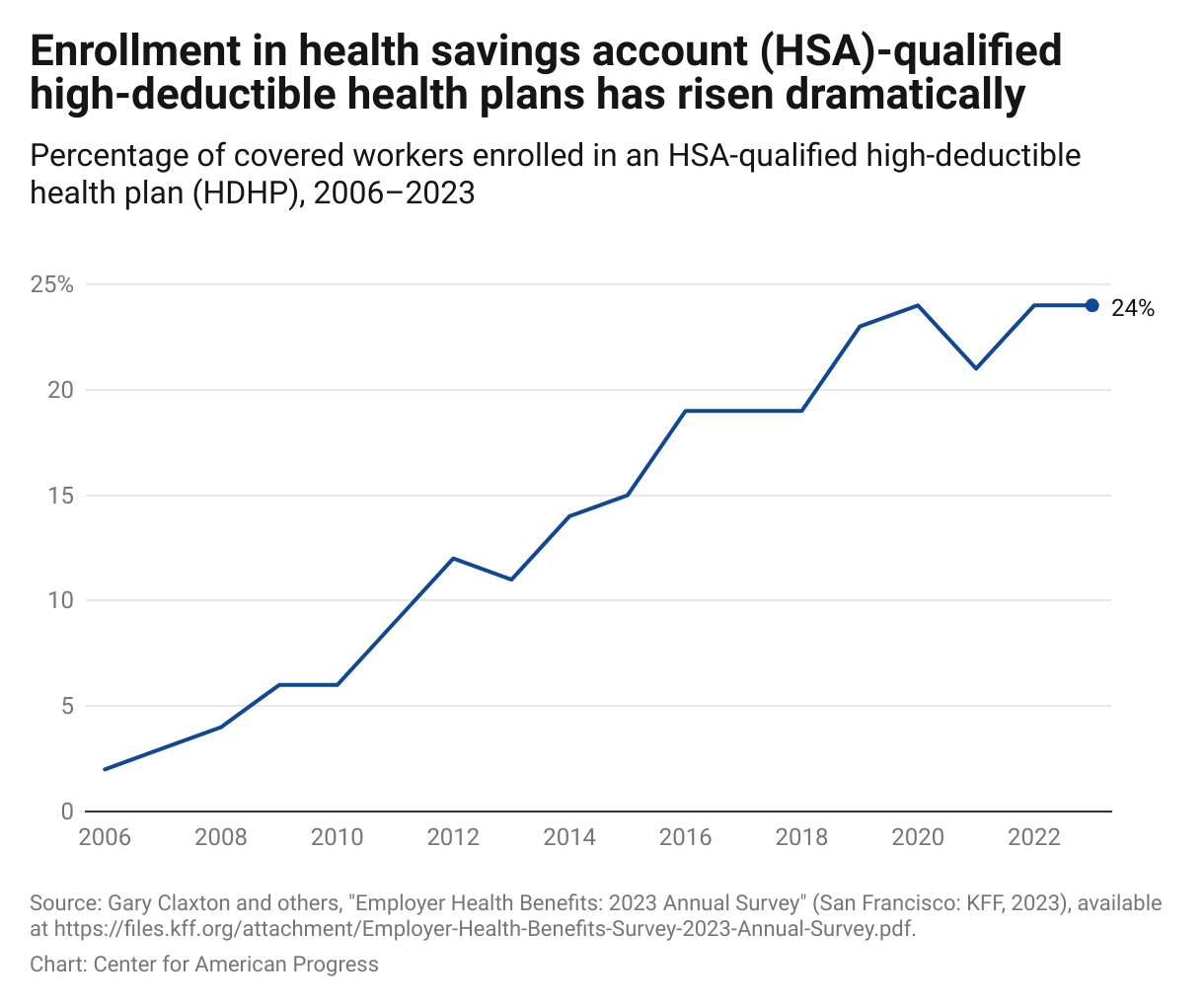

First, a quick primer. You can’t have one without the other—to even open an HSA, you must be enrolled in a qualified High-Deductible Health Plan. Think of the HDHP as the gatekeeper; it’s a health insurance plan with a higher deductible (the amount you pay out-of-pocket before insurance kicks in) than traditional plans.

The HSA, then, is your personal financial tool. It’s a special savings account where you can stash money to pay for those qualified medical expenses you’ll encounter before meeting that higher deductible. And this is where the magic—the tax magic—happens.

What Makes a Plan “High-Deductible”?

The IRS sets the rules each year. For 2024, an HDHP must have a minimum deductible of $1,600 for an individual or $3,200 for a family. But there’s also an out-of-pocket max. Your plan can’t require you to pay more than $8,050 for an individual or $16,100 for a family in covered expenses. These numbers matter because they define your playing field.

The Triple Tax Advantage: It’s the Real Deal

This is the core of it all. HSAs aren’t just tax-advantaged; they’re triple-tax-advantaged. It’s a rare and beautiful thing in the tax code. Let’s break it down.

1. Tax-Deductible Contributions

Money you put into your HSA reduces your taxable income for the year. Contribute through payroll deductions at work? Even better—those contributions are typically made pre-tax, so you never see that money on your W-2. It’s like getting an instant discount on your medical savings equal to your tax rate.

2. Tax-Free Growth

This is the superpower many people miss. Unlike a Flexible Spending Account (FSA), your HSA balance rolls over year after year. And you can invest the funds in your HSA—in mutual funds, stocks, etc. Any interest, dividends, or capital gains you earn? They grow completely tax-free. It’s a stealth retirement account for health costs.

3. Tax-Free Withdrawals

When you use the money for qualified medical expenses—think doctor visits, prescriptions, dental work, even certain over-the-counter items—you pay no taxes on the withdrawal. Zero. It’s a clean, tax-free transaction from start to finish.

Common Tax Pitfalls and How to Sidestep Them

Of course, nothing’s perfect. The IRS has rules, and missteps can be costly. A major pain point? Knowing what counts as a “qualified expense.”

Using HSA funds for non-qualified expenses before age 65 triggers income tax plus a hefty 20% penalty. After 65, you can withdraw for any reason—you’ll pay income tax, but the penalty disappears, making it function a bit like a traditional IRA at that point.

Another hiccup: over-contributing. For 2024, the limits are $4,150 for individual coverage and $8,300 for family coverage. Go over, and you’ll pay a 6% excise tax each year until you correct it. It’s a sneaky, avoidable error.

Strategic Moves: Beyond the Basics

If you just use your HSA to pay current bills, you’re leaving money on the table. The real savvy comes from playing the long game.

Consider this: pay for smaller medical expenses out-of-pocket if you can afford to. Let your HSA funds sit and grow, invested, for decades. Keep your receipts—you can reimburse yourself from the HSA for those expenses at any time in the future, tax-free. It’s a way to build a tax-free medical emergency fund for retirement, when healthcare costs inevitably rise.

And here’s a trend worth noting: more people are viewing the HSA as a critical piece of their retirement puzzle, not just a yearly healthcare slush fund. The flexibility is, frankly, unparalleled.

Is This Duo Right for You? A Quick Reality Check

The tax benefits are stellar, sure. But an HDHP/HSA combo isn’t a one-size-fits-all solution. It works best for people who are generally healthy and can comfortably cover the higher deductible if a surprise medical issue pops up. It’s also a powerful tool for the self-employed or those without comprehensive employer coverage.

If you have predictable, high medical expenses every year, a traditional plan with lower out-of-pocket costs might be a safer harbor. You have to run the numbers—premium savings from the HDHP plus the tax benefits versus your expected healthcare usage.

At the end of the day, understanding the tax implications of Health Savings Accounts and High-Deductible Health Plans is about more than compliance. It’s about seeing a financial tool for what it truly is: a unique opportunity to build security on your own terms. The tax code gives you this rare gift—a perfectly legal, triple-threat advantage. The question isn’t just whether you qualify, but how creatively and wisely you choose to use it.